The U.S. dollar continued to chug along higher last week closing at 101.57. The week was marked by volatility after Monday saw the Italian referendum being rejected.

Traders pushed the euro lower on Monday’s open but by the day’s close, the single currency was seen trending higher.

However the gains were short lived as the ECB managed to beat down the euro once again. EURUSD closed the week near a 4-day low.

On the economic front, the data last week was quiet with only second tier data coming out of the U.S.

The equity markets rose to record highs on Thursday and Friday marking one of the best weeks since the November presidential elections. The equity gains extended a month long rally for the stocks as investors hoped that stronger economic growth and fiscal stimulus spending will boost inflation higher and thus affect the short term interest rates.

Among the central bank meetings last week, the RBA and the BoC events passed off quietly. While the RBA held interest rates steady, economic data showed weakness as the third quarter GDP showed that the Australian economy contracted 0.5% more than expected.

In Japan, it was the same story as the third quarter revised GDP was pushed lower to show 0.3% increase, down from the previous estimates of 0.5%. However, the currencies continued to remain choppy with the exception of the Japanese yen. USDJPY breached 115.00 by Friday’s close.

Technical Outlook

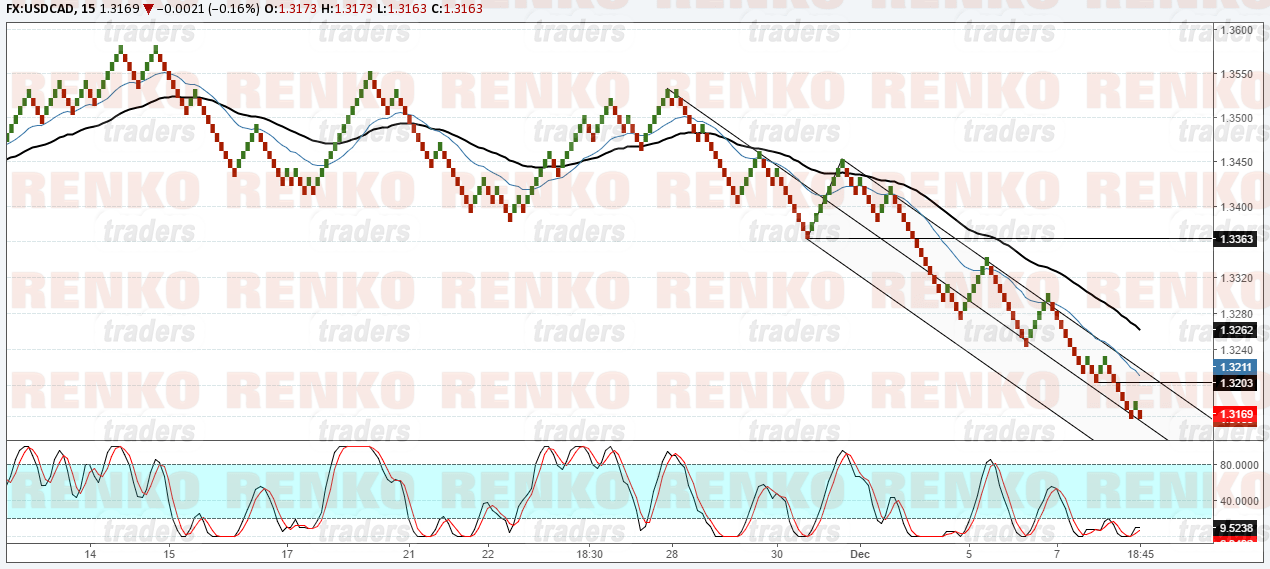

USDCAD: The dollar was weaker against the CAD as the OPEC led rally continued to keep the oil dependent currency well bid. USDCAD closed out at 1.3169. Further weakness could send the dollar lower towards 1.3150. However, watch for a potential rally as the dollar could rise above 1.3200. In this scenario, USDCAD could be seen extending its gains towards 1.3360. It is recommended to continue holding or adding to long positions above 1.3200 as USDCAD could see further upside gains in the coming weeks.

[sscl id=”1749″]

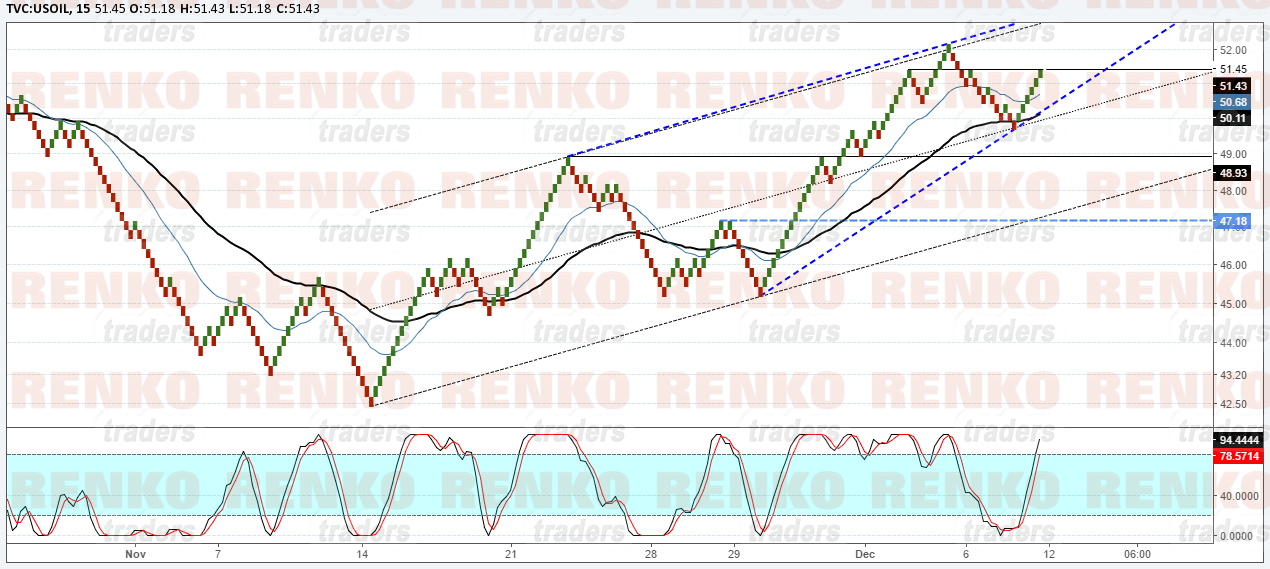

WTI Crude Oil: Oil prices have retreated after briefly trading above the $52.00 handle. The current upside could be weakening as price retest the $51.45 handle. A reversal here, supported by the bearish divergence in price could signal a near term correction towards 47.18. Look for a breakout from the ascending triangle pattern which will see the initial declines towards the $49.00 handle where support could be established. This will be a key level as prices initially hit resistance here before breaching this level on the November 30 OPEC led rally. A break out below $49.00 will see oil prices extend the declines to $47.18.

[sscl id=”1749″]

EURGBP: The euro has been trending weaker against the British pound, closing on Friday at 0.8392. However, this strong decline is likely to see some near term retracement. Initial resistance is seen at 0.8343 following which further upside could send the euro towards 0.8500 against the pound sterling. Price action is currently looking to breakout from the falling price channel, which will signal an initial rally towards 0.8343. The short term upside bias will be invalidated if price breaks down below the previous low of 0.8370.

[sscl id=”1749″]

XAUUSD: How much further will gold prices drop next week? That is the question on everyone’s mind including myself. However, the declines are unlikely to continue further without a meaningful pullback. The gold chart shows prices currently forming a double bottom at 1161.36. A bullish close from here, above 1166.00 could signal near term retracement. Initial resistance is seen at 1246 – 1251 which will be tested if there is any upside bias and above 1166.00. It is therefore recommended to look for long positions in gold above 1166.00 with the stops being covered as soon as prices break above the 1176.00 high.

[sscl id=”1749″]

Fundamental Outlook

The week ahead is dominated by the FOMC meeting where the markets are pricing in a strong likelihood of another 25 bps rate hike. This could effectively mark a second interest rate hike from the U.S. Federal Reserve. The markets will focusing on the Fed’s dot plot and staff economic projections (SEP) which will mark a major adjustment of the market’s view on further rate hike plans.

Besides the Fed’s meeting, US consumer inflation data and retail sales are likely to add some noise.

In the UK, the monthly jobs report, inflation and retail sales are due followed by Thursday’s Bank of England monetary policy meeting. No changes are expected from the BoE but the economic events could definitely shape the short term trend in the British pound. Traders should therefore pay attention to the EURGBP this week.