The long anticipated rate hikes from the U.S. Federal Reserve came last week as the central bank hiked the short term interest rates by 25 basis points as widely expected by the markets. The short term interest rates moved higher for the second time in a year and comes after a decade of low interest rate regime. The markets took the rate hike decision with cheer as the policy move was being widely expected and the markets had, since the beginning of the year been pricing in one rate hike for 2016.

The U.S. dollar continued to post strong gains edging higher to a post a fresh 14-year high. However by Friday, the dollar index was showing signs of stalling, closing with an inside bar and with a bearish pattern. With last week, the U.S. dollar index was seen posting strong gains for 6 weeks in total since the November election outcome.

The Fed’s event was clearly the main headline event last week overshadowing all othe events. Besides the Fed’s meeting, two other central bank meetings were also held last week, including the Bank of England and the Swiss national bank. Both the central banks were seen keeping monetary policy on hold.

Technical Outlook

USDCAD: From last week, USDCAD dipped slightly below 1.3150 to test the 1.3100 support level and eventually pushed higher. The rally from 1.3100 saw prices reaching to the previous broken support at 1.3370 which managed to halt the rally. Looking ahead, USDCAD could stay consolidated near the currency level for a more firm test of resistance to 1.3370. A reversal here will signal further downside towards 1.3200 support. The trend line plotted on the chart has already been broken indicating the downside bias in prices. The Stochastics oscillator is also currently plotting lower highs against the higher high in prices validating this downside view.

WTI Crude Oil: WTI Crude oil prices broke down from the rising wedge pattern last week and started to retrace back to the breakout level at $52.00. We can now expect to see a reversal near this level which will signal a downside continuation towards the initial support at $49.00. A breakdown below this level could see prices extend the declines towards $47.25. The bearish view in oil prices validates the downside bias in USDCAD meaning that the dollar could be looking weaker in the coming weeks. The Stochastics oscillator is also currently showing a bearish divergence indicating the short term decline.

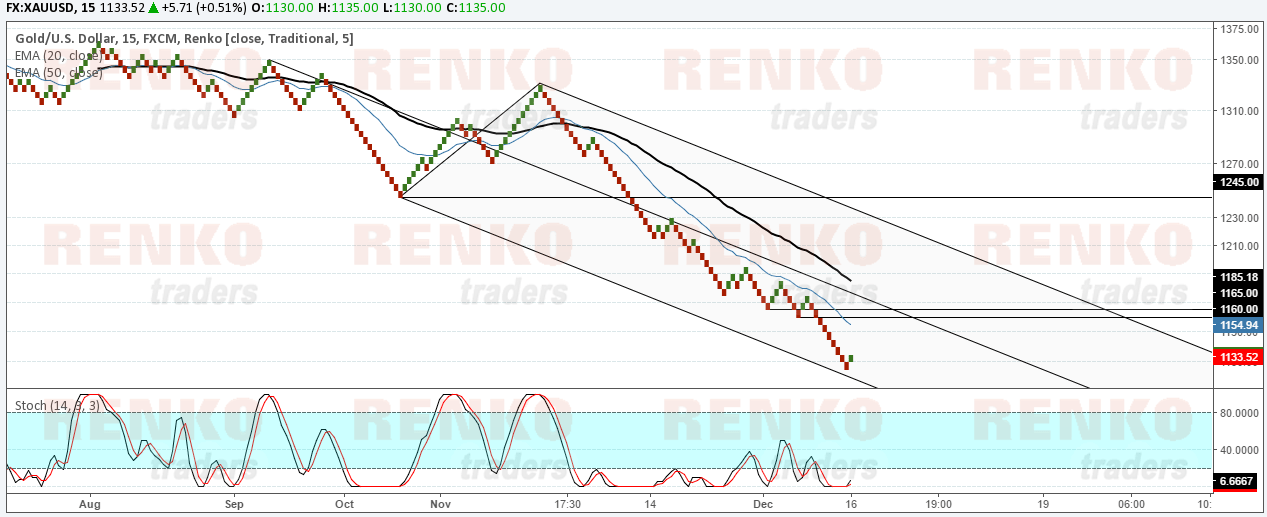

XAUUSD: Gold prices posted strong declines after the Fed hiked rates last week as price fell to fresh lows, breaking below the $1150 support level. By Friday, gold prices fell to lows of $1125. While the downside is likely to continue towards $1100, any short term gains will be validated only on a close above $1150 – $1160 handle. In this event, gold prices could be seen rising to $1245 – $1250 where resistance is likely to cap the gains in the short term. Currently, price has posted a low while the Stochastics remains in strongly oversold levels. Look for price to make a higher low which will be the clue for further upside. Long positions could be taken bove 1150, targeting 1250 as a result, while to the downside, the bearish trend could see price slipping to 1100 support.

USDJPY: The USDJPY remains elusive showing a strong momentum led rally over the past few weeks. By Friday’s close USDJPY formed a double top at 118.50 which could signal a correction if price continues lower. The trend line will be the key as USDJPY needs to break this rising trend line. Technical support is seen at 106.00 which will be the key level of interest to the downside. The bearish view is yet again validated by the bearish divergence on the Stochastics, but a confirmation is required by way of breaking the rising trend line.

Fundamental Outlook

Looking ahead, the markets will be slowing down as traders take a break with the end of the year holiday season. Trading volumes are likely to remain low in the final two weeks of this year. On the economic front, next week’s big event will be the Bank of Japan’s monetary policy meeting. The central bank is expected to keep monetary policy unchanged with interest rates steady at -0.10% and the bank’s QE purcahses being unchanged.

Elsewhere, GDP figures will be coming out for the third quarter. Data includes Q3 GDP figures from the U.S., the UK and New Zealand followed by Canada’s monthly GDP figures. In the U.S. the final revised GDP is expected to be revised higher to show 3.3% quarterly GDP growth, higher than the second estimates of 3.2%. In the UK, no changes are expected to the final Q3 GDP figure while in New Zealand, the third quarter GDP is forecast to rise 0.8%, slower than the second quarter GDP print.